Hello friends! Here’s my monthly take on five most interesting developments in transport energy trends. What I try to do each month is select stories, studies and other interesting items that you may not have seen elsewhere but that really represents an important issue or trend that I think you would want to know about. Or I try to poke behind the hype to provide a deeper understanding of what’s happening. Items I selected this month include:

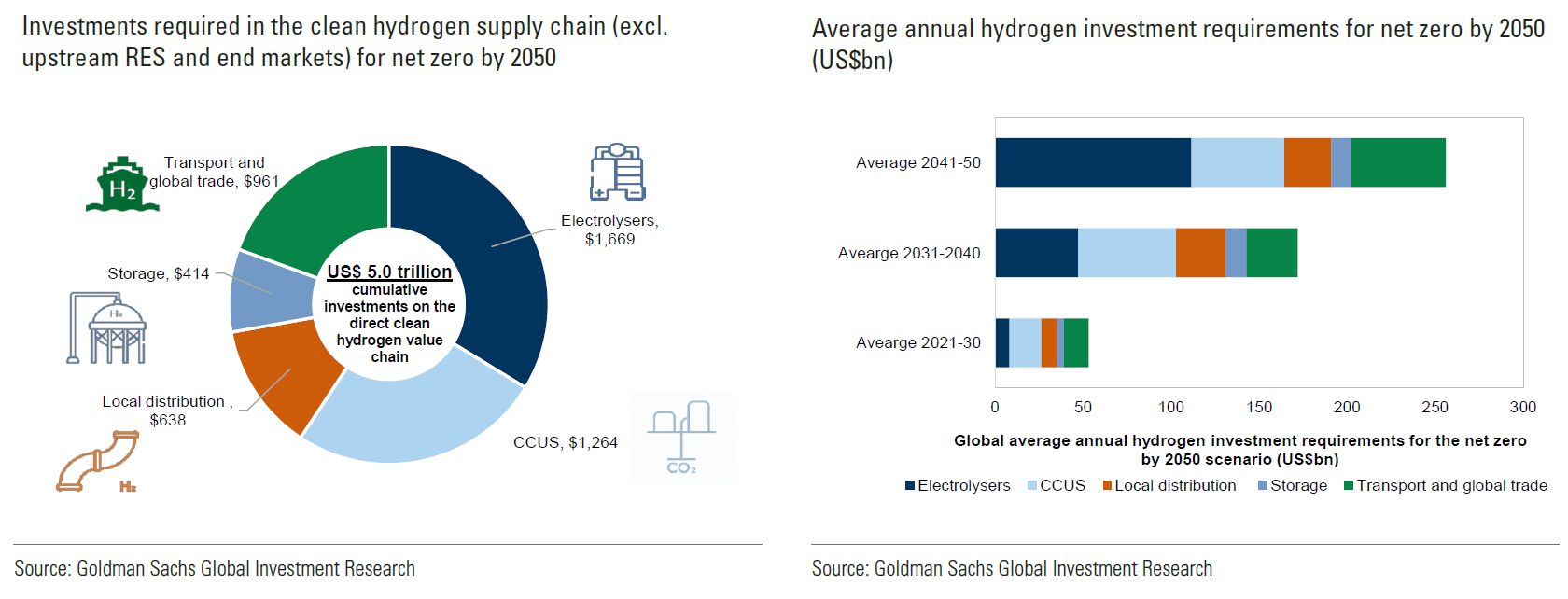

Business Chief: Goldman Sachs – Clean Hydrogen Transformational for Net Zero – Goldman Sachs in a recent report and noted in this article says clean hydrogen can develop into a major global market, impacting energy supply, and accounting for up to 30% of global hydrogen volumes crossing borders. The firm’s report notes that, “We estimate US$5.0 trillion of cumulative investments in the clean hydrogen supply chain will be required for net-zero, while the total addressable market (TAM) for hydrogen generation alone has the potential to double by 2030 (to US$250 bn) and reach more than US$1 tn by 2050.” Investment requirements are broken out in the figures below.

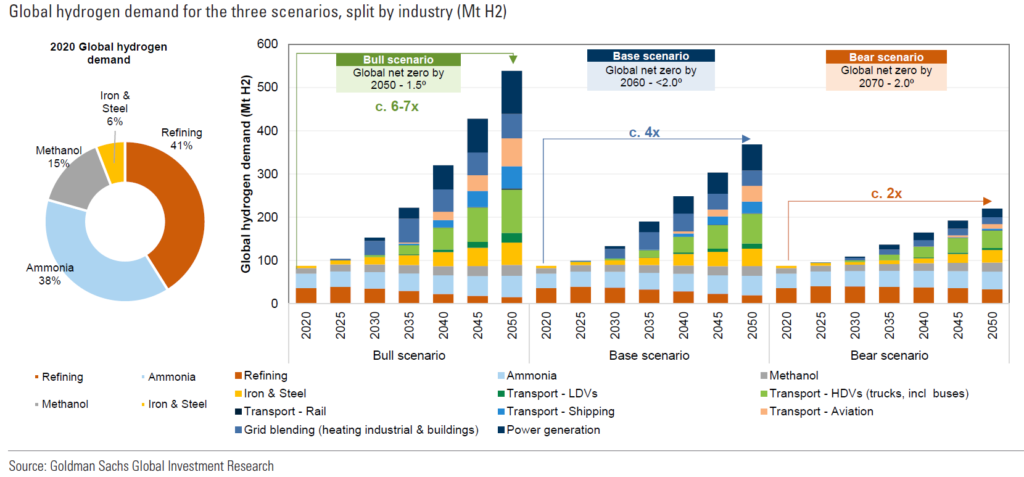

Using its own net-zero model, Goldman Sachs has devised three hydrogen scenarios based on 1.5 degree Celsius global warming, one with well below 2C, and one on 2C (bull, base and bear scenarios). The findings, summarized in the figure below, suggest that under all three scenarios global hydrogen demand increases at least 2-fold on the path to net-zero, from 2-fold in the bear scenario to 7-fold in the bull scenario.

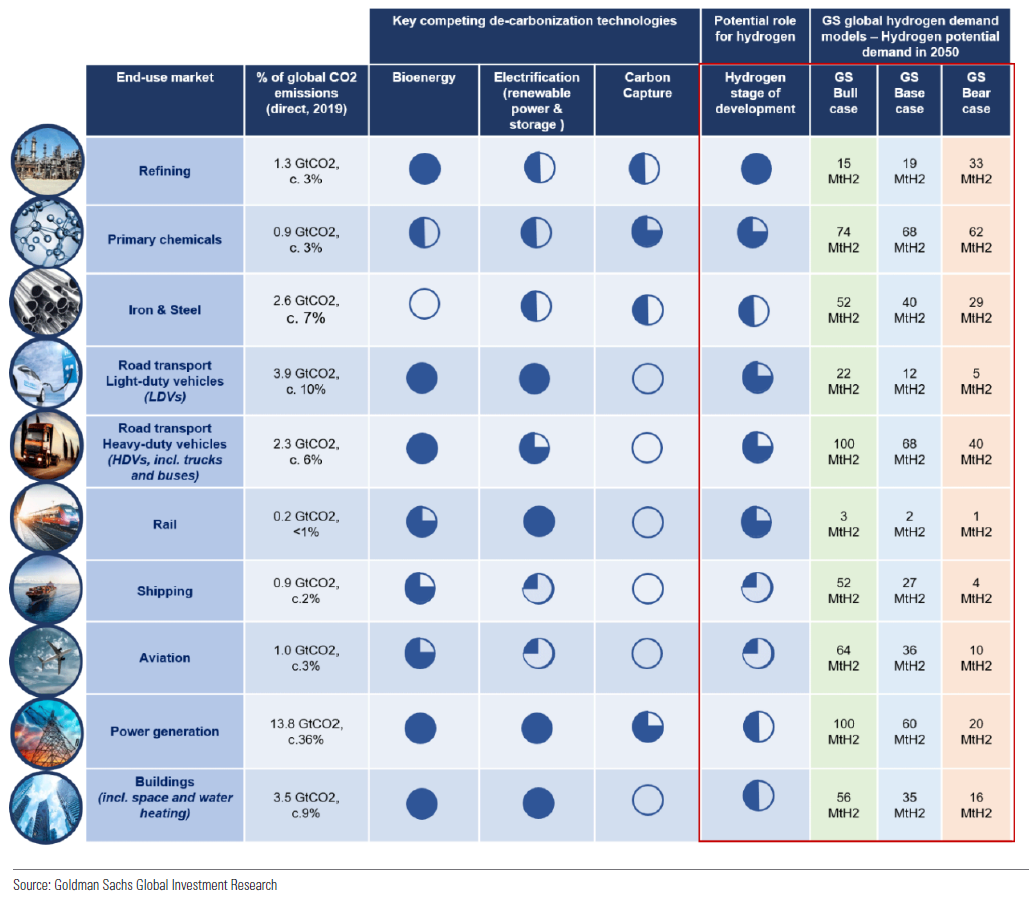

The figure below breaks this demand out further by key addressable markets and compares to other key competing decarbonization technologies such as bioenergy (biofuels), electrification and carbon capture.

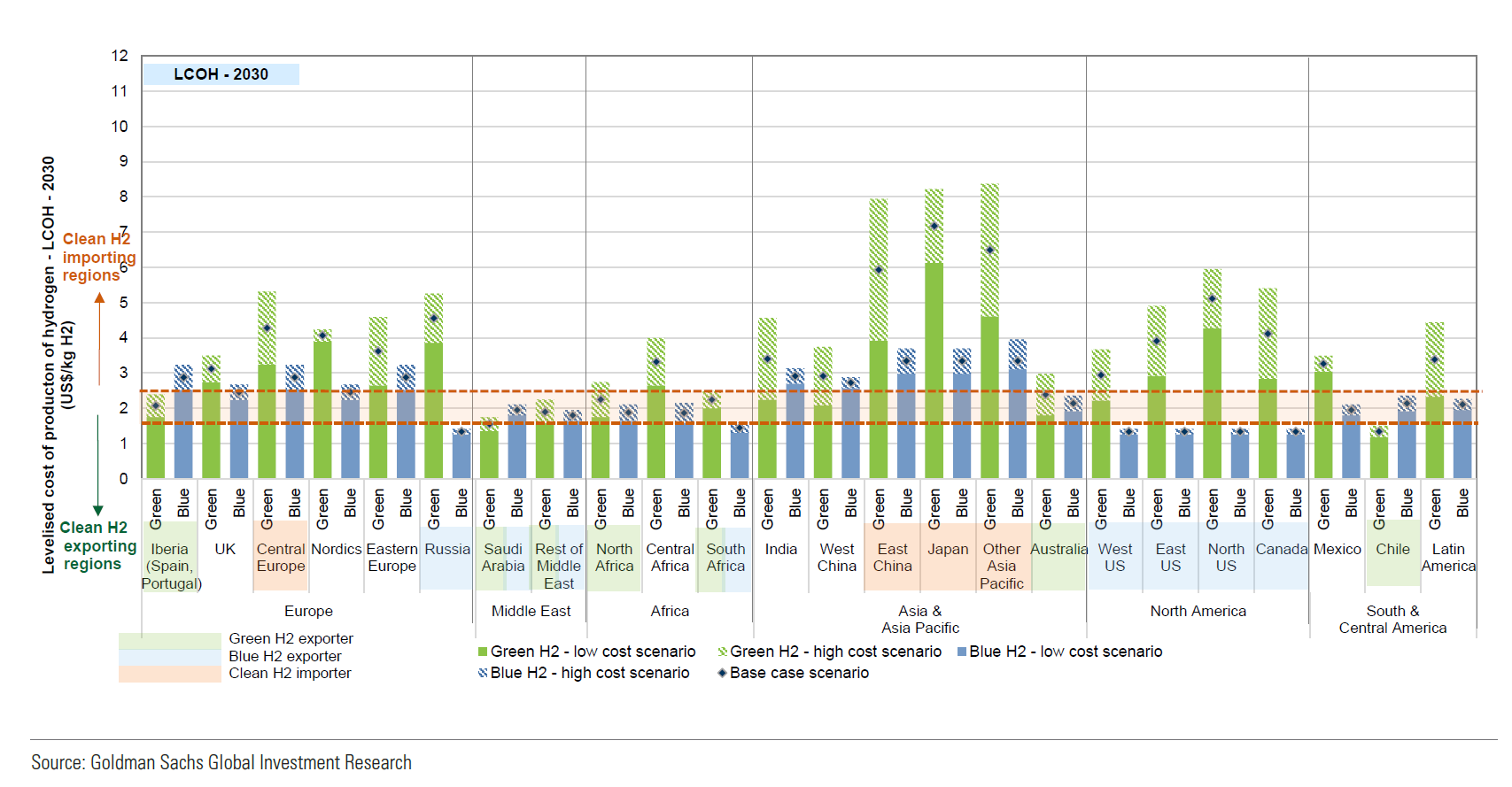

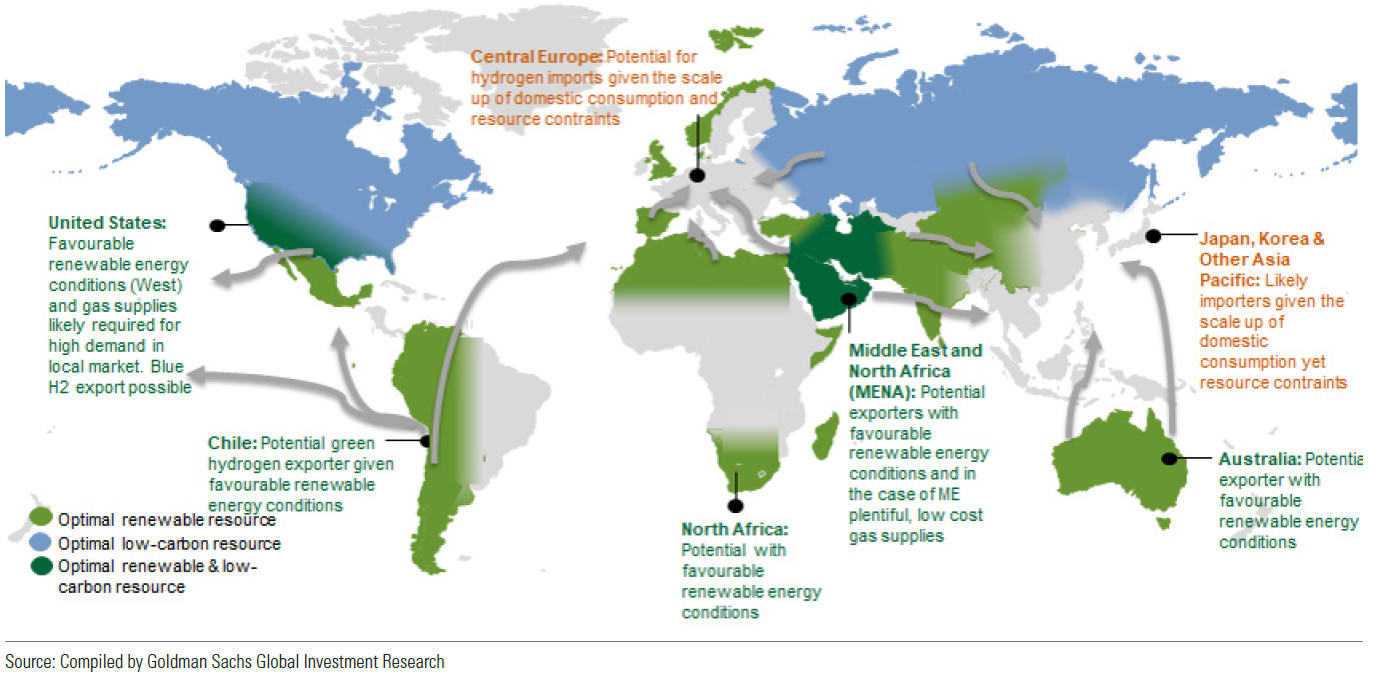

As shown in the figure below, MENA, Latin America, Australia and Iberia could emerge as key clean hydrogen exporting regions, while Central Europe, Japan, Korea and parts of East China could emerge as key importing regions.

The map below shows the potential evolution of a global market for hydrogen.

2. Emerging Tech Brew: “It’s All Coming at The Worst Time:” How Sky-High Nickel Price Could Hamper EV Efforts – We’re hearing a lot about lithium and cobalt supplies, but the war in Ukraine has raised another supply chain concern that impacts EVs: nickel availability. Since Russia’s invasion of Ukraine on Feb. 24, three-month nickel prices on the London Metal Exchange soared from less than $25,000 to more than $100,000 per ton for a brief period last week.

The article notes that nickel-rich chemistries are popular among battery makers because the metal has historically provided higher energy density at a lower cost than alternative cathode materials. Some battery makers have actually been trying to increase the share of nickel in the battery chemistry in order to use less cobalt, which is typically more expensive and often mined under dangerous conditions.

NMC batteries—the dominant type of lithium-ion battery used in EVs today—have cathodes made up of nickel, manganese, and cobalt. NCA batteries, another common type, are made of nickel, cobalt, and aluminum. Nickel can make up as much as 80% of the cathode materials in both of these chemistries.

While companies with long-term nickel contracts in place may not feel immediate cost increases, one source noted in the article that this uncertainty comes at a time when companies and governments in Europe and North America are making big investments in domestic EV production and battery supply chains. Moreover, much of the new nickel-mining capacity set to come online in the next few years is in Indonesia, but Chinese companies have already signed agreements for much of that new supply, Sanderson said. And China could get a hold of Russian nickel as well given current developments. That adds additional uncertainties particularly American and European automakers.

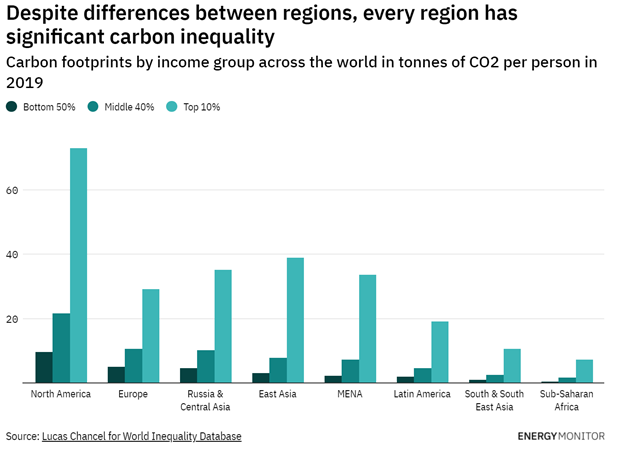

3. Energy Monitor: Targeting the Super-Rich Could Contribute to Net Zero – This article highlights a recent study which found that income is a significant predictor of household consumption-related environmental impact. With an increase in income, both direct emissions, such as those from fuel and electricity use, and indirect emissions – from food and goods, for example – increase.

According to data from a study for the World Inequality Database (WID), the top 10% wealthiest people are responsible for almost half of individual CO2 emissions globally, with the top 1% contributing close to 17%. In contrast, the bottom half of people are responsible for just 12% of individual carbon emissions. Based on an input-output framework that represents the interdependencies between different economy-environmental sectors, the same study estimates that 60–70% of the global carbon footprint can be traced to individual consumption.

While there are significant differences in historical CO2 emissions between countries – with the US and Europe contributing the most to global emissions – the trend of carbon inequality persists within every region and is shown in the figure below. Yes, carbon inequality is a thing.

What to do? To target high-consuming households, researchers suggest targeting high-income households. But that’s not easy. For example, consumption-based taxation tends to be absorbed rather easily by high-income households but hurt lower-income households.

4. Agriland: EU to Use CAP Funds to Boost Biomethane Output – I see, so far, two potential beneficiaries of the terrible war in Ukraine: China’s acquisition of cheap, cut-rate natural gas from Russia, and to a lesser extent, a recommitment and expansion of biomethane (i.e., renewable natural gas or RNG) in the EU to offset natural gas supply losses from Russia. This article bears my theory out. Under REPowerEU, the European Commission is seeking to diversify gas supplies and speed up the roll-out of renewable gases, among other objectives, which officials say can reduce EU demand for Russian gas by two-thirds before the end of the year.

The Commission plans to use funding under the Common Agricultural Policy (CAP) to double the planned production of biomethane by 2030 in order to reduce the reliance on gas from Russia. This new plan would lead to the creation of 35 billion cubic meters of biomethane per year by 2030 (double a plan under Fit for 55 that envisaged 17 billion cubic meters per year). The article notes that to achieve this, the commission says that EU member states’ CAP Strategic Plans should channel funding to biomethane production produced from biomass sources, including agricultural wastes and residues in particular. The CAP Strategic Plans are currently before the European Commission for review, having been submitted by member states before the end of last year. The Commission is due to revert to member states with comments on these plans before the summer.

5. The Wall Street Journal: ESG May Be an Antitrust Violation – The opening sentences of this op-ed from Mark Brnovich, Attorney General of the U.S. state of Arizona, really caught my attention:

“The biggest antitrust violation in history may be in plain sight. Wall Street banks and money managers are bragging about their coordinated efforts to choke off investment in energy. It’s nearly impossible to raise money to explore for oil and gas right now, and we may all be experiencing rising energy costs because of this market manipulation.”

What’s the argument? Brnovich lays it out:

“The biggest banks and money managers seek to implement a political agenda, such as compliance with the Paris Climate Accord. Then a group mobilizes: Climate Action 100+, for example, comprised of hundreds of big banks and money managers that together manage $60 trillion. The group uses its coordinated influence to compel companies to shut down coal and natural-gas plants. The activism can include pushing climate goals at shareholder meetings and voting against directors and proposals that don’t comport with the agenda, even if other decisions may benefit investors. Firms report their plan to carry out these activities back to Climate Action 100+ headquarters. This helps ensure maximum coordinated effort toward the common goal of overhauling the energy industry.”

It will be interesting to see whether this goes anywhere, or whether this could become a multistate investigation and/or litigation. The bottom line though is that there is evidence emerging that energy-states are beginning to push back against banks that are pushing ESG initiatives. For example, In November, 15 US states – responsible for more than $600 billion in funds – wrote an open letter to the banking industry in which they threatened to withdraw their business from financial institutions that boycott fossil fuel companies. And several states, including Texas, are considering legislation that would prohibit the state as well as local governments in Texas from doing business with any companies that divest from fossil fuels. The battle lines are beginning to be drawn, and the banks do not have all the leverage as it turns out.

Tammy Klein is a consultant and strategic advisor providing market and policy intelligence and analysis on transport energy to the auto and oil industries, alternative fuels industries, governments and NGOs. She writes and advises on petroleum fuels, biofuels and other alternative fuels, and fuels policy, market and technology issues.

{kind=link}