{kind=link}

IRA: How the U.S. May Eventually Overtake the EU in Sustainable Aviation

03.23.23 | Blog | By: Philippe Marchand

The European Commission wants to be seen as the undisputed leader in the fight against climate change, with ambitious plans for net-zero-emissions in 2050, guiding the world toward a sustainable future. The European Parliament is usually even more enthusiastic in terms of regulatory ambition, and so are the environmental NGOs, behind both bodies. The EU Member States regularly take a dimmer view about these generous initiatives, as they have to face local constituencies that may argue about the consequent undue burden, considerably slowing down the whole regulatory process.

A good case to consider is the introduction of sustainable aviation fuels (SAF) in air transport, deemed by all experts of this sector as the major and only serious approach to decarbonize this mode of transport.

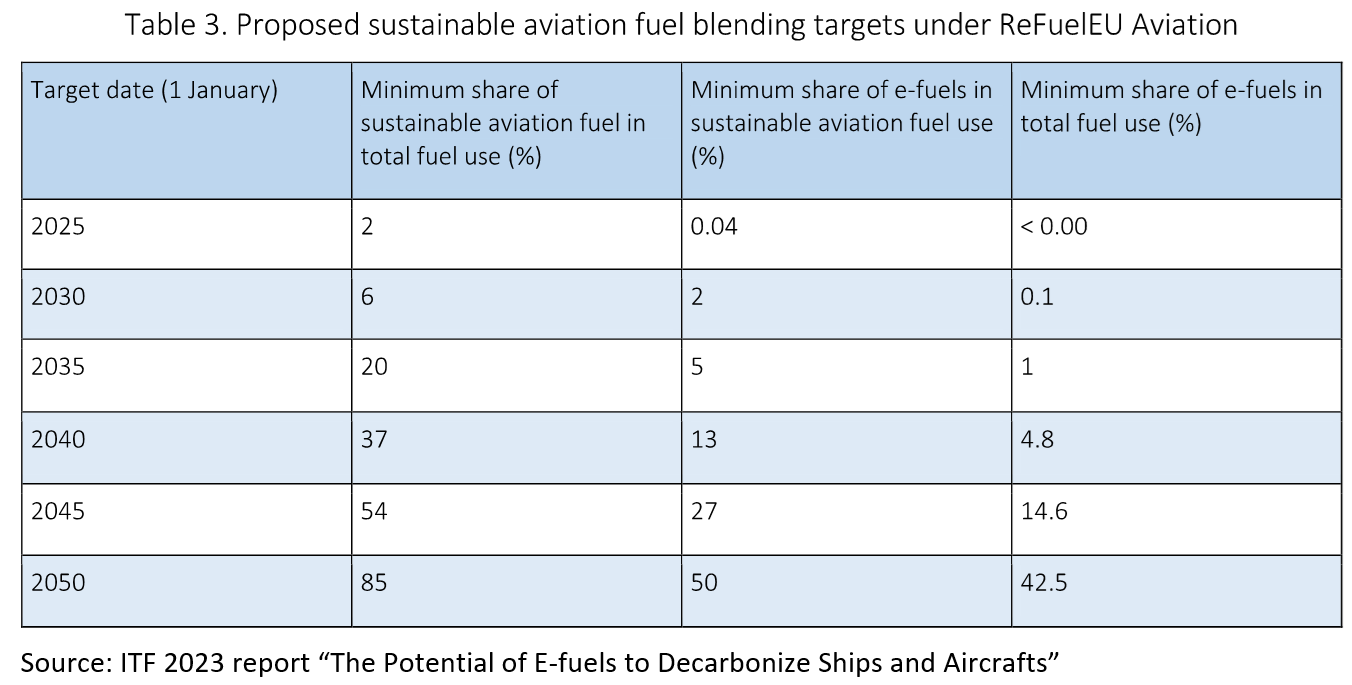

More than a decade of solid R&D, numerous private (industry-wide) and public stakeholders’ working groups and advocacy, eventually yielded a comprehensive and long-term, hopefully stable, regulatory proposal, esoterically named ReFuel EU Aviation. It calls for the mandatory incorporation of SAF in commercial aviation fuels as from 2025, with a complete flightpath to 2050 as shown in the following figure.

Should SAF, once qualified for international usage (anywhere, on any plane) by ASTM International, with a detailed and straightforward technical specification (ASTM D7566, the low-carbon equivalent of ASTM D1655, used for commercial aviation fuel), be left under the responsibility of the fuels industry to supply, with the proper certificate of quality and sustainability, assuming CO2 emission reduction is the key deliverable, the runway would be clear for take-off. But such a level-playing field is not fit for Europe.

Not only do you notice in the table above that there is a sub-mandate for e-fuels, produced from renewable electricity-derived hydrogen and CO2 (direct capture or industrial), thanks to Germany’s lobbying, but this clearly ignores the technology-neutrality approach.

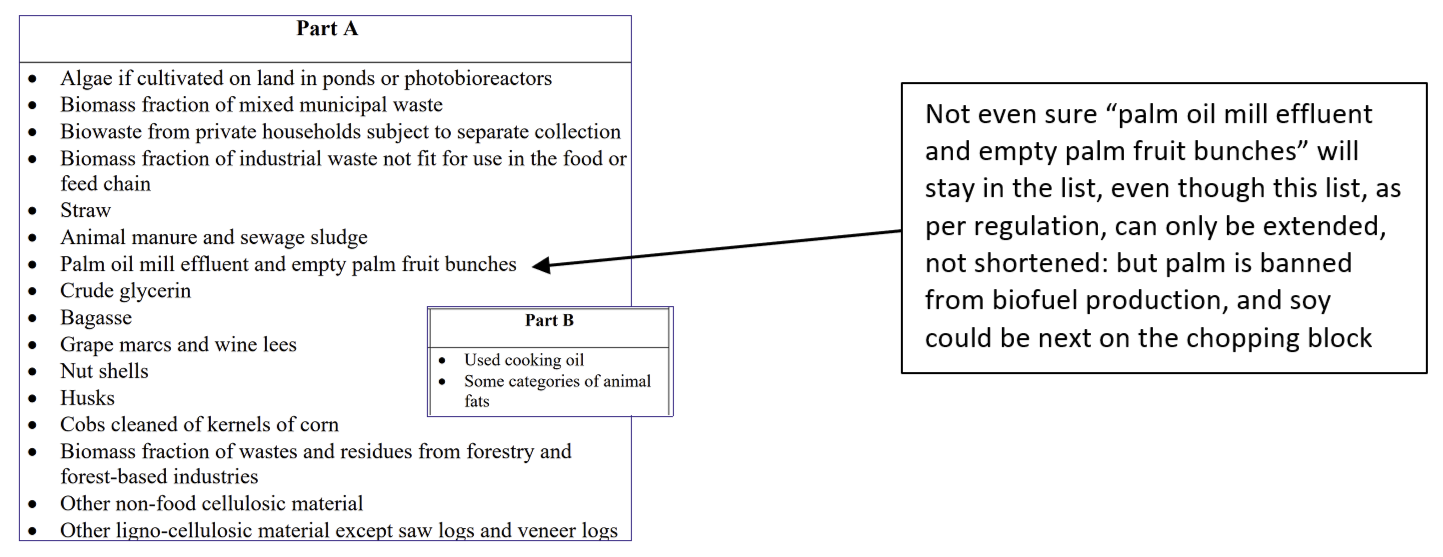

But sustainability goes deep in terms of excluding, banning, excommunicating. Airlines’ lobbying, eagerly accepted by the European Commission, has succeeded in allowing only residual raw materials to be eligible for SAF production. Is it useful here to mention that environmental NGOs are strongly anti-biofuels in the EU?

And not any waste or residue can be eligible: there is a catalog, the Annex IX of the Renewable Energy Directive (RED), with two parts, A and B, each with different mandatory constraints and listing some exotic raw materials:

Source: A. Salimbeni, BIKE, citing the Renewable Energy Directive, February 2023

As someone rightfully said during the recent 2023 CERAWeek in Houston, TX: Europe is about sticks, and the U.S. about carrots.

In the U.S., the first carrot was awarded to industry by the California Air Resources Board, in the form of the Low-Carbon Fuel Standard (LCFS), a generous carbon credit philosophy that allows SAF to be produced reasonably competitively to fossil jet-fuel, kicking-off the market. Second is the federal Inflation Reduction Act (IRA), offering generous (again) subsidies to green and innovative industries, which should spur SAF production, especially if the U.S. government has success with its Grand Challenge to have 10% SAF in commercial aviation fuel by 2030. Note that this objective is twice the European one. And the eligibility criteria are less stringent, which is not surprising as the U.S. road biofuel regulation, the Renewable Fuel Standard (RFS2), is also less demanding that the EU Renewable Energy Directive (RED).

In the short-term, mandates are usually stronger than incentives to kick-start a market. And industry in the EU is indeed building SAF production capacity, roughly to match the 2030 objectives so far. But the true challenge lays beyond 2030. The United Nations International Civil Aviation Organization (ICAO) made its members (countries) agree to a long-term aspirational goal of zero emissions by 2050, which means that the so far fragmented, nascent, and regional SAF market will eventually become global, making SAF a commodity, like ethanol, traded on a world-wide basis. This is technically possible due to the fungible nature of SAF (hydrocarbons, similar to those found in fossil-based jet-fuel but produced from renewable or low-carbon resources by various pathways).

In such a global market, mass production will come from the most cost-efficient production zones. As long as reducing CO2 emissions is the key demand to global airlines and aviation fuel suppliers, making production more difficult and more costly by severe regulatory demands, on feedstock nature for instance, like the ones described above for ReFuel EU Aviation, will eventually turn the EU into a SAF consuming zone, not a producing one. This inconvenient fact has not escaped Airbus CEO Guillaume Faury, who publicly conveyed earlier this year his fears that the EU regulation will move SAF production away from the EU in the longer term. You can trust airframe and engine manufacturers to think long-term.

The best is the enemy of the good, goes the conventional saying. This applies to sustainability as well. Reducing CO2 emissions is the priority, and solutions should first be judged according to this objective. Fine-tuning on other criteria can come at a later stage once emissions are phased down and aviation gets back in the fray of acceptable modes of transport, from the environmental viewpoint.

Philippe Marchand is a Bioenergy Steering Committee Member of the European Technology and Innovation Platform (ETIP).