Hello friends! Here’s my monthly take on five most interesting developments in transport energy trends. What I try to do each month is select stories, studies and other interesting items that you may not have seen elsewhere but that really represents an important issue or trend that I think you would want to know about. Or I try to poke behind the hype to provide a deeper understanding of what’s happening. Items I selected this month include:

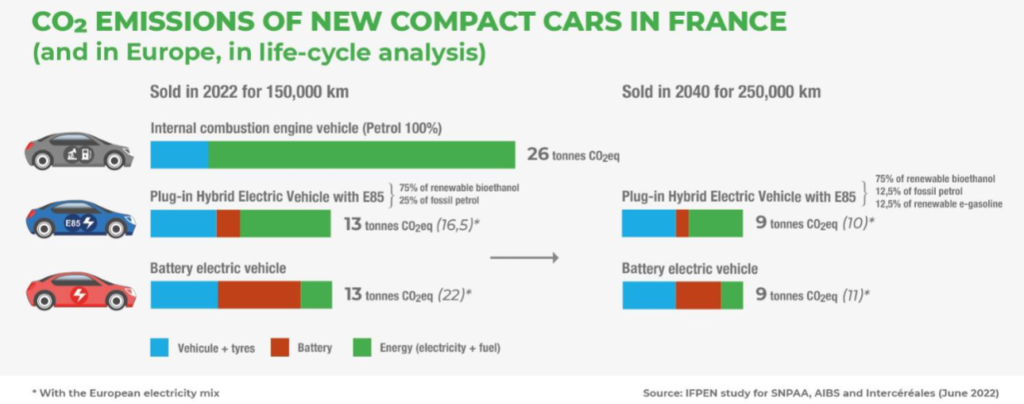

1. Bioethanol Carburant: A New IFPEN Study Confirms the Essential Role of Bioethanol in Reducing Automotive CO2 Emissions – According to a new study from IFPEN in France, plug-in flex-fuel hybrid vehicles running on E85 fuel with up to 85% renewable ethanol are just as climate-friendly as EVs. IFPEN researchers measured and compared the lifecycle GHG emissions of vehicles powered solely by petrol, plug-in flex-fuel hybrids running on E85 and all-electric cars. Researchers factored in, for example, all GHG emissions in connection with the vehicle and its battery (from manufacture to recycling) as well as the energy used (production, refinery, transport, distribution and combustion). The findings were applied to French and European electric power mixes.

This comparison, applying to 2022 with projections for 2040, shows that plug-in flex-fuel hybrids running on E85 operating 40% of distance travelled as an EV are at least as climate-friendly as all-electric vehicles, with the French electric power mix which is already low-carbon, and even more with the average European mix, which has a higher carbon footprint. This is shown in the figure below. (See related commentary on this by Philippe Marchand here.)

The EU will begin a three-way negotiation (“trilogue”) this fall among the EU Parliament, European Council and European Commission on CO2 standards for cars and consider what the European car fleet will look like as from 2035. The proposal from the Commission adopted by the Parliament will require a 100% reduction in CO2 from vehicles by 2035. Right now, the policy militates toward 100% EVs, but there could be an opening during the trilogue for other non-EV solutions that can reach carbon neutrality.

To that end, this week, automotive companies, fuels manufacturing companies and industry associations implored EU policymakers to carefully consider the approach in setting final CO2 standards. They point out that “the geopolitical landscape has changed dramatically, with implications for energy and raw material dependencies. This is likely to have an impact on the speed and economic efficiency of the electrification of the new light-duty vehicles fleet.” Battery raw material prices have increased, supplies are scarcer (see below), and EV charging infrastructure is developing in the EU but not at a sufficient enough pace.

What’s the solution? Similar to the one of the points made in the IFPEN study, the companies and industry groups note that:

“The fuels industry has set out that production of sustainable, advanced and synthetic fossil free fuels can be ramped up. A needed enabler for this to occur is the clear recognition in regulation and society that ICE, HEV and PHEV vehicles exclusively using sustainable renewable and synthetic fuels can be very low in GHG footprint or even fully climate neutral. Significant volumes can be made from waste and residue feedstocks and from renewable energy sourced in EU and imported. Highly credible academic studies demonstrate that this combination can equal that of the EVs in terms of decarbonisation of road transport…

Since the transition towards a fully electric mobility will be progressive, sustainable biofuels, renewable fuels and e-fuels are a reliable solution to reduce emissions of the transport sector in the short, medium and long term, ensuring at the same time the use of the existing fleet (so-called legacy fleet) and infrastructure. Electrification and CO2-neutral fuels should be seen as complementary solutions.”

It will be interesting to see how the trilogue handles this, if at all.

2. EURACTIV: Parliament Backs E-Fuels, Higher EU Transport Decarbonisation Target – Meantime, the EU Parliament last week voted to approved revisions to the Renewable Energy Directive (RED III) to: 1) increase the EU’s transport emissions reduction target from 13% to 16% by 2030 which it expects to achieve through the use of advanced biofuels and e-fuels; 2) more than double the target for synthetic fuels to 5.7% by 2030, including a 1.2% sub-target for the maritime sector; 3) increase the renewable energy target to 45% by 2030 (the Commission’s original proposal was 40%; and, 4) retain the 7% cap on first generation feedstocks but will classify soybean oil as a “high-risk” indirect land use change (ILUC) feedstock meaning they cannot be used for compliance with RED. The Parliament may also consider moving up the target end date of 2030 to 2023. There will be, as with the CO2 standards, a trilogue negotiation to agree the final policy sometime later this year.

3. Wall Street Journal: Battery Metals Mining Has a Resource Nationalism Problem – “The green revolution is handing additional leverage to countries where metals like copper and nickel are being dug up. Expect them to use it.” Case in point as noted in this article: Chile. The country voted earlier this month on a new constitution one provision of which would have made mining in the country much more difficult and costly.

It would have granted indigenous groups, including those who live near northern Chile’s vast lithium deposits, more autonomy over ancestral lands and require their consent for new projects. More importantly, it would have raised mining taxation to about 59%. The new constitution was defeated, but the trend toward exercising tighter control of resources, especially those related to battery and EV manufacturing, continues.

The article notes that in addition to Chile, Bolivia and Mexico are also tightening mining regulations, according to S&P Global. Serbia revoked Rio Tinto’s license for its Jadar lithium project in January due to concerns about the potential environmental impact. Indonesia, the world’s top nickel producer, may impose a tax on some product nickel exports this year. Expect more countries to follow suit.

Meantime, prices of battery-grade lithium carbonate in China are currently nine times higher than they were in the beginning of 2021, according to Rystad Energy. The International Energy Agency estimates that lithium demand from EVs and battery storage will need to grow 40-fold by 2040 to meet Paris Climate Accord goals. Nickel, cobalt and graphite demand will need to rise as much as 25-fold.

Dozens of lithium mines are in various stages of development in Canada and the United States, according to the New York Times. The Times notes, “But most of these projects are years away from production. Even if they are able to raise the billions of dollars needed to get going, there is no guarantee they will yield enough lithium to meet the continent’s needs.” That’s just for North America, not other top EV markets, such as in the EU.

4. Health Effects Institute: Comprehensive New Report Details Two Major Air Pollutants and Related Health Impacts in More Than 7,000 Cities – The world’s biggest cities and urban areas face some of the worst air quality on the planet, according to a new report published by HEI (Health Effects Institute). The report, Air Quality and Health in Cities, released by HEI’s State of Global Air Initiative, provides a comprehensive and detailed analysis of air pollution and global health impacts for more than 7,000 cities around the world, focusing on two of the most harmful pollutants; fine particulate matter (PM2.5) and nitrogen dioxide (NO2).

The report, using data from 2010 to 2019, found that global patterns for exposures to the two key air pollutants are strikingly different. While exposures to fine particulate, or PM2.5 pollution tend to be higher in cities located in low- and middle-income countries, exposure to nitrogen dioxide, or NO2, is high across cities in high-income as well as low- and middle-income countries. This is reflected in the table below.

Source: HEI, September 2022

PM2.5 and NO2 are both heavily linked to vehicle emissions, though that is not the only source. The report mentions low emission zones, improved fuel quality and efficiency and improving traffic flows. Electric vehicles are not mentioned directly. However, the need to eliminate these emissions and the fact that, in some cases, they are not being reduced is part of what is propelling EVs as a long-term solution. One can argue the merits of EVs from the GHG-reduction point of view, and oh, they do, but there’s no denying the tailpipe benefits of EVs, which matter just as much to regulators around the world.

5. DNV: Maritime Forecast to 2050 – DNV has released a forecast for maritime to 2050, including an outlook for fuels and ships, finding that (just as with other sectors) the maritime industry will go through “a period of rapid energy and technology transition that will have a more significant impact on costs, asset values, and earning capacity than many earlier transitions. Shipowners are already experiencing increasing pressure to reduce the greenhouse gas (GHG) footprint of maritime transport.”

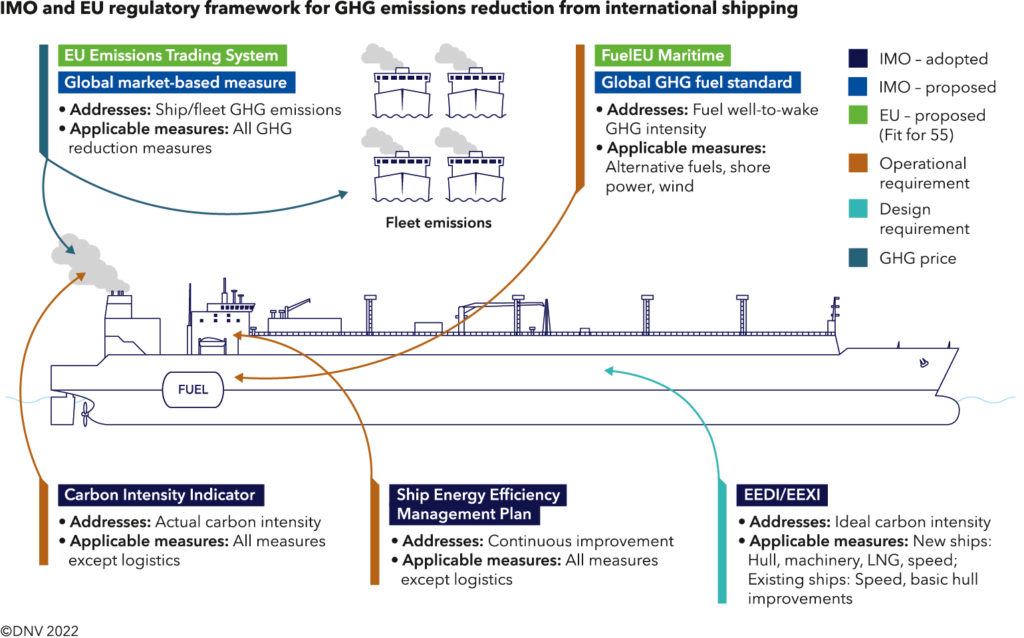

Part of that pressure is attributed to pending regulations at the International Maritime Organization (IMO) and the EU Commission, summarized in the graphic below. DNV notes that from 2025 the focus will shift to calculating lifecycle GHG emissions, creating an additional urgency for a green supply chain to control emission costs.

DNV notes the IMO Strategy will be revised in 2023, possibly strengthening its emission-reduction ambitions. This will be followed by developing the next wave of regulations including market-based measures setting a price on CO2 and a requirement to account for well-to wake GHG emission intensity of fuels. Meantime, the EU has proposed to include shipping in the EU Emissions Trading System (EU ETS) and has proposed the FuelEU Maritime regulation which aims to increase the use of carbon-neutral fuels through an increasingly stringent well-to-wake GHG intensity requirement. These proposals may be finally adopted later in 2022 and take affect from 2024 and 2025, respectively.

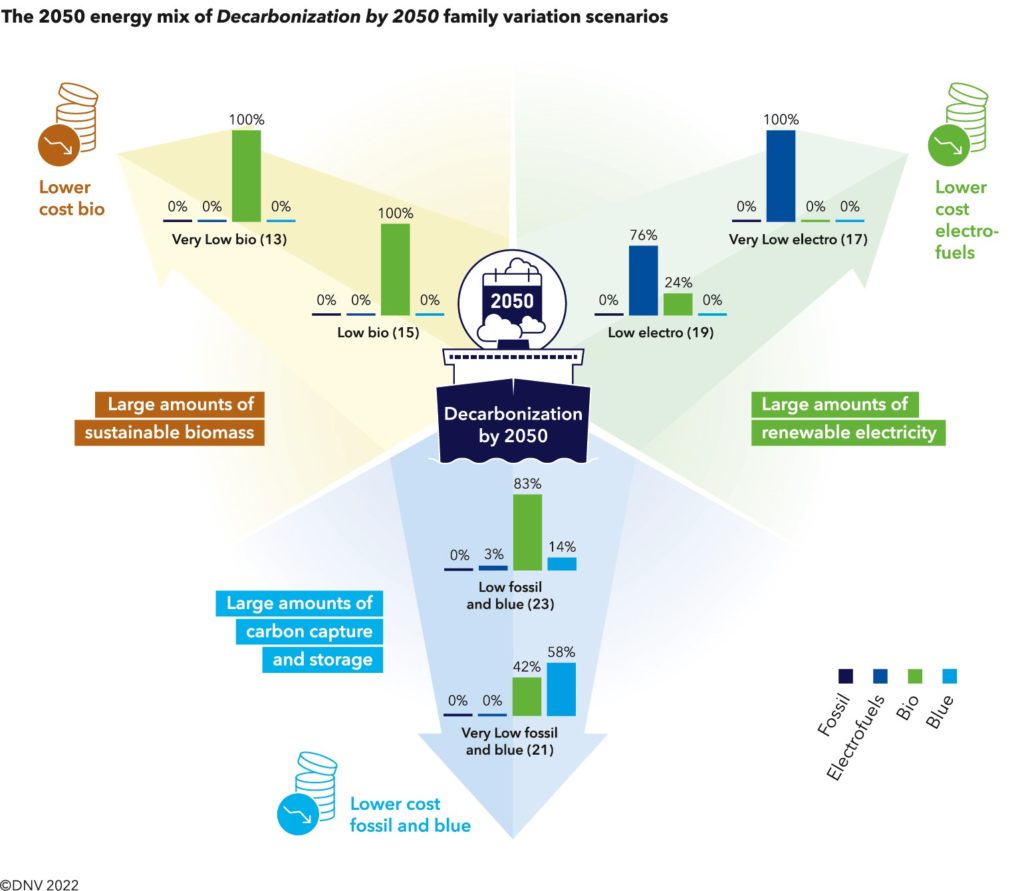

What could this mean for fuels? DNV estimates that by 2030, 5% of the energy for shipping should come from carbon-neutral fuels, and that by 2050, if the sector were to totally decarbonize, fuels dominating the energy mix for shipping could be bio-MGO, bio-LNG, e-ammonia, blue ammonia and bio-methanol. All fossil fuels would be eliminated. Grid electricity provides around 7-8% of total energy, while 92-93% comes from carbon-neutral fuels. This is shown in the figure below.

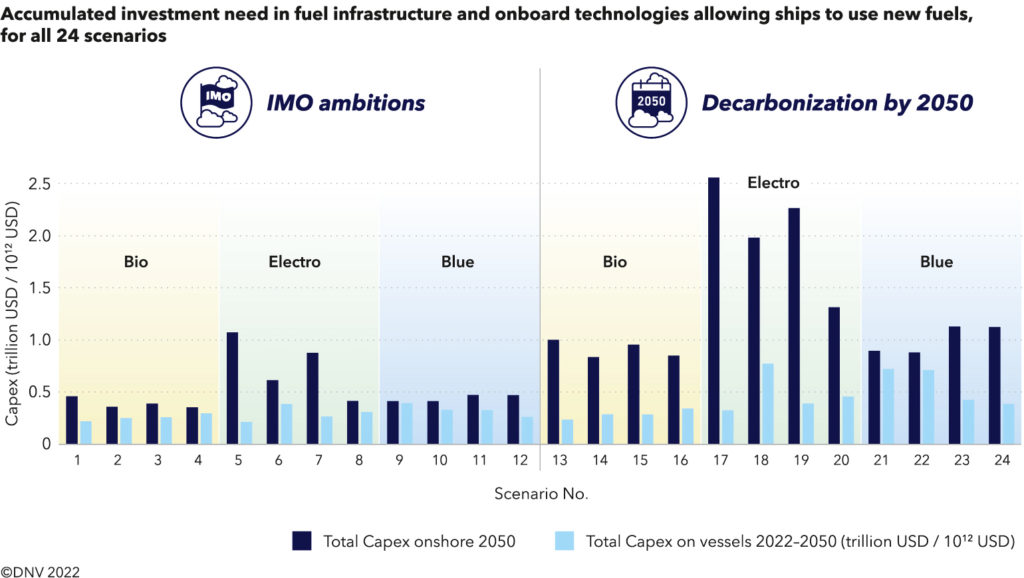

Where it gets tricky (always) is with the investment that would be required – and that would run into the trillions for some scenarios (like electrofuels) DNV ran for the study, shown in the figure below.

Tammy Klein is a consultant and strategic advisor providing market and policy intelligence and analysis on transport energy to the auto and oil industries, alternative fuels industries, governments and NGOs. She writes and advises on petroleum fuels, biofuels and other alternative fuels, and fuels policy, market and technology issues.

{kind=link}