{kind=link}

Whoa! Renewable Diesel Projects Explode Around the World

04.05.22 | Member Reports & Posts | By: Tammy Klein

Members may recall in my last post on renewable diesel (RD or HVO) (see post Sept. 8, 2021) that I focused primarily on the many project announcements in the U.S. For this updated post, I focused on global projects. Most of these RD projects are HVO-based, with some exceptions, such as the Velocys Bayou Fuels project. The newly announced projects, especially in Europe, are eyeing the burgeoning sustainable aviation fuel (SAF) market, which I’ll cover in a separate post next month.

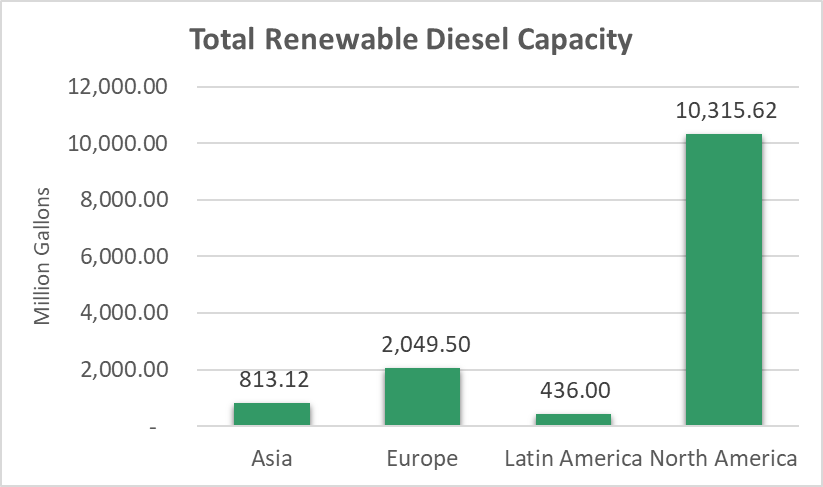

For this research, I counted 79 projects with a total capacity of 13 billion gallons (39.75 million metric tons). The figure below shows total renewable diesel capacity by region.

Source: Transport Energy Strategies, April 2022

I’m sure I’ve missed some, and if I have, please let me know (especially those members directly involved in the space) and I’ll update my data. The project spreadsheet not only includes capacity data, but a pivot table and charts in gallons and metric tons. For the first time, I’ve created a global map to plot these facilities and I’ll continue to update it over time.

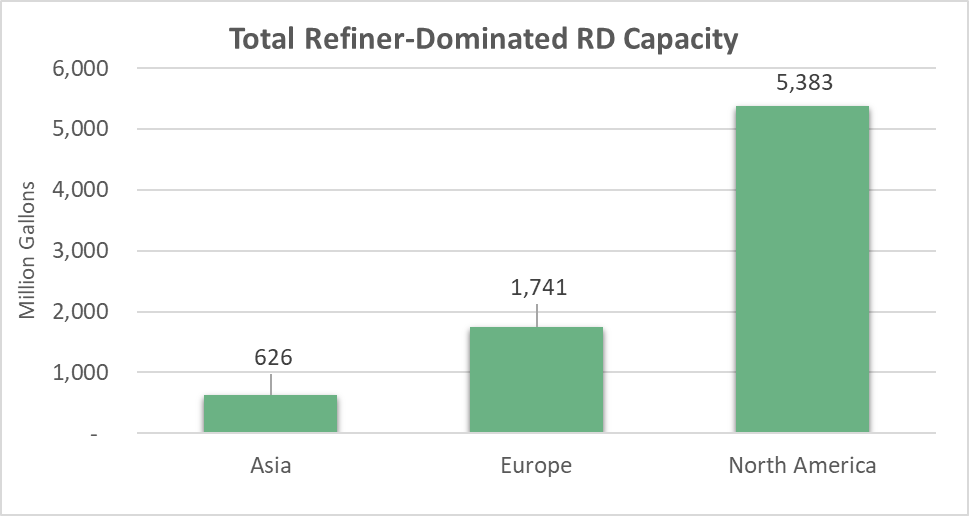

More than half the projects are based in North America, and there are several new projects in Canada. There are new projects in Europe as well, with announcements from PKN Orlen (Poland), Tupras (Turkey), Shell and OMV. All the new projects are refiner-backed. In fact, as the figure below shows, refiners dominate the space, representing about 60% of all projects.

Source: Transport Energy Strategies, April 2022

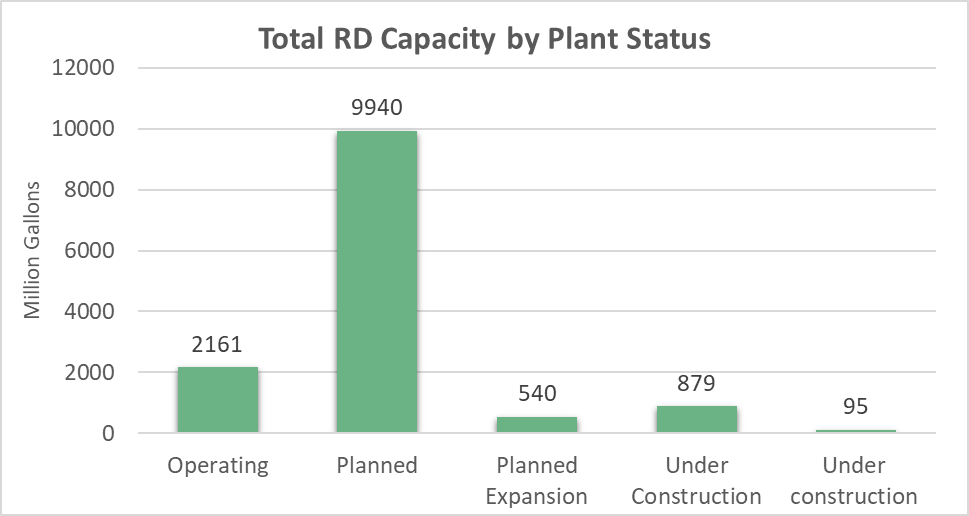

The figure below shows RD capacity by plant status. A little over 2 billion gallons of capacity is operating with much of the remainder planned.

Source: Transport Energy Strategies, April 2022

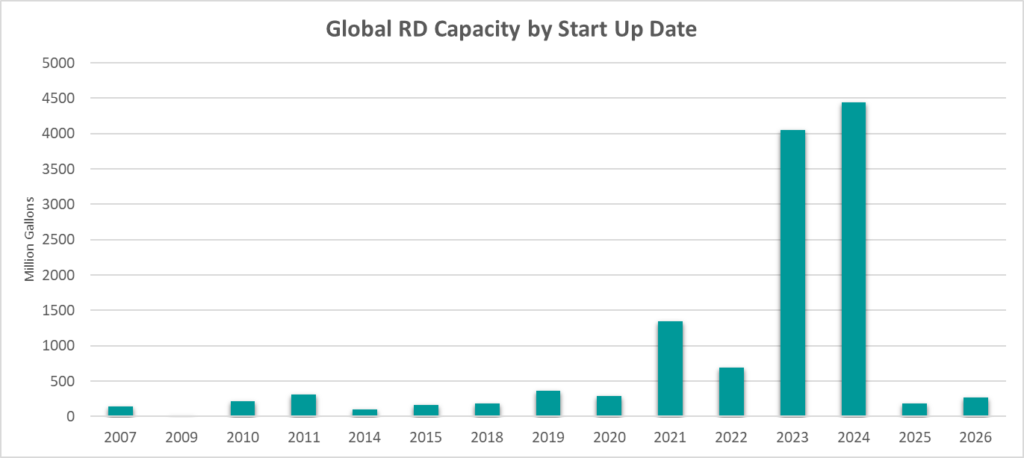

Almost all the planned capacity is targeted to come online in the 2023-2024 timeframe, shown in the figure below. I find that a bit aggressive overall, especially considering some projects have been announced just in the last few months.

What kinds of feedstocks are producers looking at? Generally, soybean and canola oil (especially for Canadian projects), rapeseed in Europe and lots of used cooking oil (UCO). Projects in China have no compunction at all about using palm oil imported from Malaysia and Indonesia – certified or not. A project in Brazil would use domestic palm oil produced in the Amazonas province. The ECB project in Paraguay plans to use pongamia. UPM is developing carinata for one of its plants. The Velocys Bayou Fuels project is gasification-based and will use woody biomass as the feedstock. But largely, projects will rely on UCO, animal wastes and soybean, canola and rapeseed oils.

In the September 2021 post, I said there would be several strategies producers will use to manage the risk this presents. One of them is joint ventures and other such agreements to secure feedstock. That continues to happen. For example, Marathon has partnered with Neste on its Martinez, California project, and one reason is feedstock. It also concluded a deal for feedstock with ADM in December 2021. Valero’s partner in Diamond Green Diesel, Darling Ingredients, recently concluded a deal for UCO from Chick-fil-A, the U.S.-based restaurant chain.

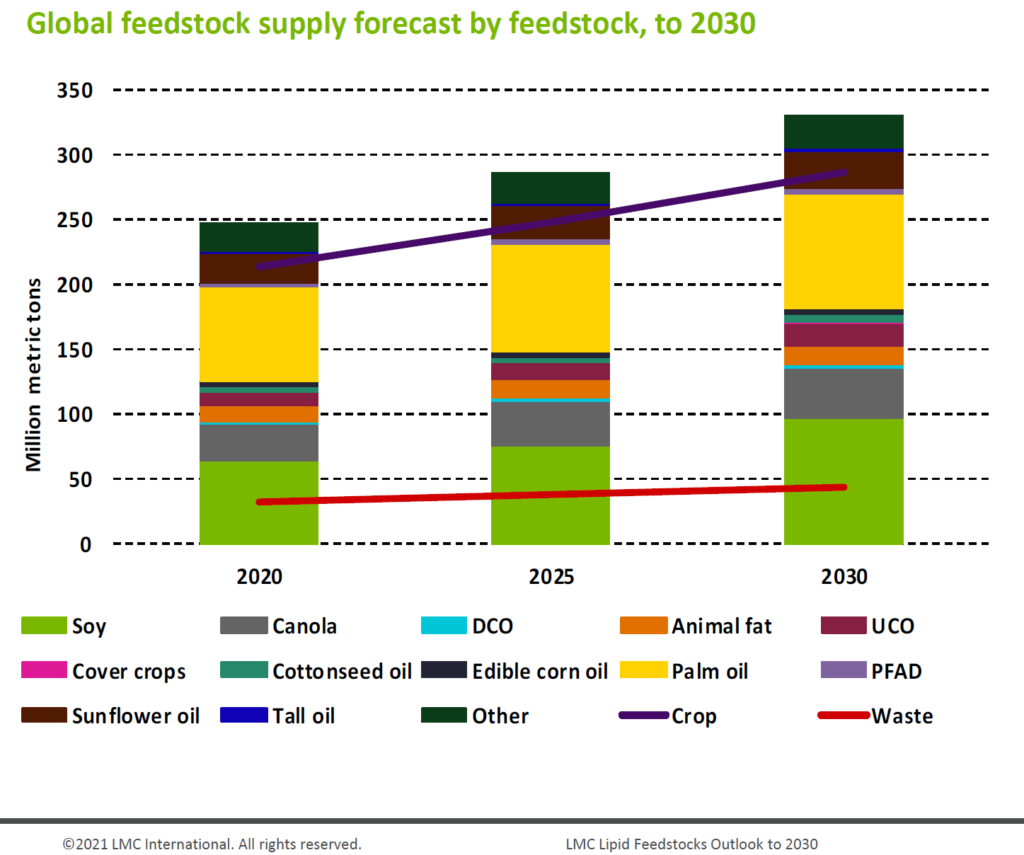

Will there be enough feedstock? I think it’s going to depend. The figure below, taken from a recent study prepared for the Advanced Biofuels Association in the U.S. provides a forecast to 2030.

What jumps out to me is just how much producers will be reliant on feedstocks such as soybean and palm oil. Soybean oil does not have the best carbon intensity (CI) score under programs such as the California Low Carbon Fuel Standard (LCFS), and palm oil is a “no go” in the U.S. and EU under the Renewable Fuel Standard (RFS2) and Renewable Energy Directive (REDII/III), respectively. Moreover, there is some UCO and animal fat. This study notes that supply chains for feedstocks like UCO can be developed. However, that is already happening in countries such as China. I think the carinata- and pongamia-back plants will be interesting to watch in terms of opening the door to alternative and yet commercial feedstocks.