While the direction of vehicle powertrain policy and strategy is firmly oriented towards full battery electric vehicles (BEVs), the results of Emissions Analytics’ latest testing and lifecycle modelling suggests that hybridisation may prove to be the dominant outcome, whether intended or not. As real-world emissions results collide with consumer preference and fiscal reality, the efficiency of hybrids in reducing carbon dioxide (CO2) emissions is likely to shine through over the next decade, even if BEVs and other new technologies come to dominate in the longer-term.

Put another way, at the moment it appears that battery electric vehicles (BEVs) are neither sufficiently clean nor a strong enough consumer proposition to achieve mass adoption without significant subsidy. They are certainly not zero emission, not least due to the construction process and tyre wear emissions. Hybrids, in contrast, reduce tailpipe CO2 emissions materially now – albeit somewhat less than BEVs – and have few utility disadvantages for consumers. Therefore, would it be optimal to follow a hybridisation strategy for, say, the next ten years and then segue to BEVs after that, once they are cleaner and have fewer consumer disadvantages?

The typical objection to this is that BEVs already in the fleet will automatically become cleaner as the grid decarbonises. While this is true, the greatest source of CO2 from BEVs is in the manufacture, which is fixed and incurred upfront. Therefore, every BEV manufactured now may crystallise enough CO2 today to outweigh the subsequently lower CO2 of operation, compared to typical hybrid vehicles.

Taking the latest sales figures for new cars from the UK’s Society of Motor Manufacturers and Traders (SMMT), and putting them together with recent test results for exhaust and non-exhaust emissions from Emissions Analytics, it possible to evaluate the progress in decarbonisation.

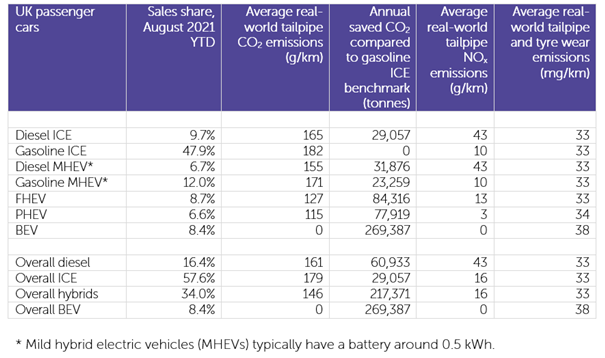

Before turning to CO2, it can immediately be seen that BEVs deliver little overall advantage for air quality. While NOx emissions remain positive for internal combustion engines (ICEs), the levels are significantly lower than for earlier models. This is true to the extent that, if the car fleet were made up entirely of these latest diesel and gasoline cars, there would be no air quality legal violations. For particle mass emissions, exhaust filters on ICEs typically reduce emissions to less than 1 mg/km. In contrast, tyre emissions from ICEs are around 32 mg/km over a lifetime, whereas the BEV tyre wear rate – other things being equal – are 21% higher at 38 mg/km. Adding exhaust and non-exhaust emissions together, BEVs are slightly higher emitting than ICEs and full hybrid electric vehicles (FHEVs).

With BEVs not required for air quality compliance, their primary environmental purpose is CO2 reduction. The table below estimates the CO2 emissions saved compared to the benchmark gasoline ICE for each alternative powertrain, based on 16,000 km of annual driving and the latest market shares of each. The greatest aggregate CO2 reduction is from BEVs, which have 8.4% market share. Hybrids, collectively, with 34.0% market share, account for around three-quarters of the reduction of BEVs.

These BEVs include around 5.5 million kWh of battery capacity, compared to 1.0 million kWh in all the hybrids together. Therefore, for every kWh of battery capacity, BEVs delivered 3.0 g/km of CO2 reduction, compared to 13.7 g/km for hybrids, both judged against the gasoline ICE benchmark. In other words, hybrids have been 4.6 times more efficient at reducing CO2 as a function of the currently constrained battery material supply.

Had the battery material from the 92,420 BEVs sold been used in hybrids – assuming average battery capacities of 60 kWh and 2.6 kWh respectively – an additional 2.1 million hybrids could have been built, enough to cover all new cars sold in the whole of 2021 in the UK. In that hypothetical scenario, the CO2 reduction from the annual operation of the hybrid vehicles would be 940 kilotonnes greater than from the BEVs.

To analyse more fundamentally the differences between the powertrains, it is necessary to consider lifecycle CO2 emissions, including vehicle manufacture, operation and end-of-life processing. To that end, Emissions Analytics has developed its own proprietary model; for the purposes of this analysis the key assumptions are:

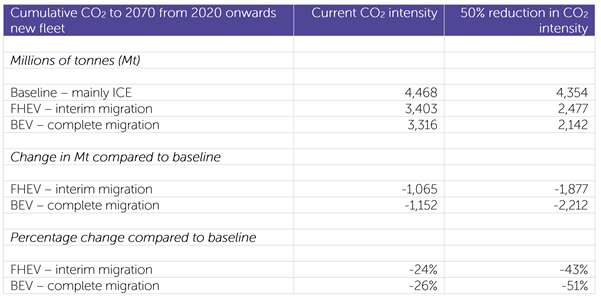

Considering the cumulative CO2 emissions to 2070, it is possible to compare six different scenarios as shown in the table below. The three powertrain scenarios are an ICE-led baseline, a direct migration to BEVs, and an interim switch to FHEVs until 2030 and then migration to BEVs. Each of these scenarios has two versions: one calculated based on current CO2 intensity of electricity generation and BEV manufacture, the other with that intensity reducing by 50% from 2030.

The reason for BEVs being hardly better than FHEVs on current CO2 intensity is that the manufacture emissions of the vehicle and battery are still relatively high, and the average grid electricity across Europe still includes significant gas and coal.

Therefore, we can deliver an extra 8% point reduction in CO2 compared to the baseline by switching straight to BEVs, if a 50% reduction in CO2 intensity is achieved from 2030. According to the fifth carbon budget under the UK’s Climate Change Act, the country can emit 1,725 million tonnes of CO2-equivalent between 2028 and 2032. The added benefit given by the direct migration to BEVs is over 10% of that carbon budget – which demonstrates how every percentage point of reduction in CO2 is important.

On the surface of this analysis, BEVs look like the optimal strategy, even though the gap to the FHEV strategy is closer than reported elsewhere. However, this neglects consideration of risk. Rolling out hybrids would be relatively low risk due to limited resource requirements, consumer resistance and taxpayer subsidy requirement. Furthermore, the BEV estimates of CO2 reduction are sensitive to many factors, including:

Each of these could have a material impact on the analysis and resulting CO2 reduction, both positively and negatively. However, as high-certainty methods of CO2 reduction are a pressing policy need, it may be better to ‘bank’ the lower-risk 24% reduction from ten years of hybrids, and then migrate to BEVs and other lower-CO2 powertrains.

Returning to the topic of currently scarce battery materials, the FHEV strategy requires 39 GWh of battery capacity for vehicles sold in the ten years to 2030. In contrast, the BEV strategy requires 570 GWh, or 15 times more. From a practical, ethical and geopolitical point of view, this is significant.

There is, further, a paradox with BEVs: once bought, from a CO2 point of view it makes sense to drive them a lot so the embedded emissions in the construction can be amortised across the maximum usage. It may even be better to drive incremental miles in the car rather on some forms of public transport. This is, therefore, linked to the question of taxing BEVs such there are no perverse incentives to drive on the road more, and creating replacement revenues for the declining taxes on gasoline and diesel.

Putting together this rate of CO2 reduction and the current utility compromises, it suggests that BEVs are not yet good enough value a product to get rapid adoption without significant subsidy. With new internal combustion engines now sufficiently clean that they are not contributing to air quality violations and the readily available alternative in hybrids, it appears that the optimal policy is to concentrate on them for the coming years while BEVs and other low-CO2 powertrains get ready for mass adoption. Greater competition would be good for consumers in the long term, especially where greater proportions of the added value in the vehicles arise domestically, whatever the country. Vast sums of taxpayer subsidy – billions, if not tens over billions, of pounds over time – could also be avoided.

Failing this, it is likely that we end up at hybridisation by another route: at the household level. This is because consumers may hold on to old ICEs to cover longer journeys, heavier payloads, sporty driving and the like. These older vehicles may also have higher NOx emissions, being Euro 6 prior to the introduction of Real Driving Emissions, or earlier. Governments may try to force these off the road through higher taxation, but this is unlikely to work as the low depreciation rates of these older vehicles will make for cheap motoring in almost any scenario.

In summary, surely it would be better to take the pragmatic route and hybridise everything as soon as possible?

This conclusion is not dissimilar from that articulated in a facsheet from the International Council on Clean Transportation in July 2021, which said, “Hybridization can be utilized to reduce the fuel consumption of new internal combustion engine vehicles registered over the next decade, but neither HEVs nor PHEVs provide the magnitude of reduction in GHG emissions needed in the long term.”

But, the numbers suggest we replace “can” with “should”, to lock in the CO2 savings now.